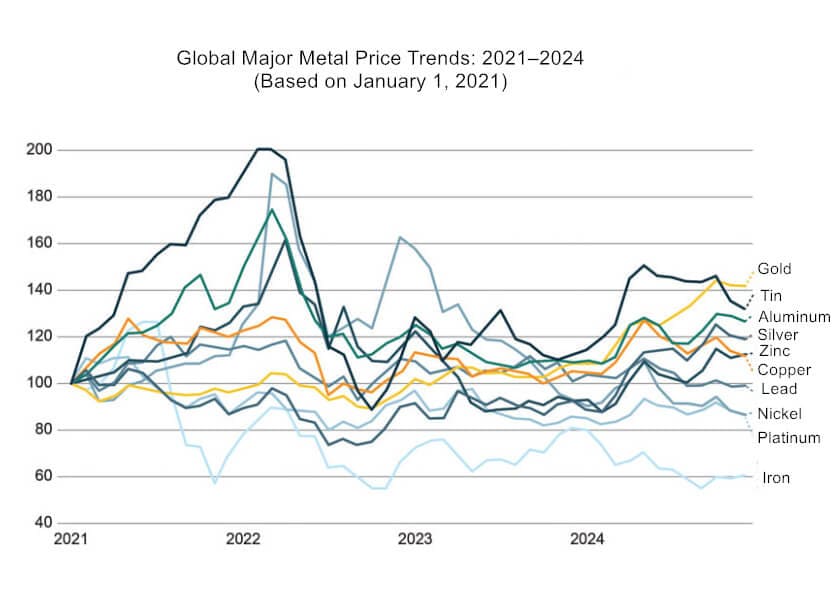

The mining and metals sector is undergoing a profound transformation amid the global energy transition and shifting geopolitical dynamics. This analysis outlines the ten key trends that will shape the industry in 2025.

1. Deepening Fragmentation of Mineral Supply Chains

Geopolitical tensions are accelerating the fragmentation of critical mineral supply chains. The U.S.-China rivalry continues to intensify, with the U.S. imposing 25% tariffs on key Chinese mineral imports, while China tightens export controls on gallium, germanium, and antimony. Further restrictions on mining & refining tech exports may follow.

Impact

- Increased price volatility & supply uncertainty

- Financing challenges for new projects

- Vertical integration becoming a competitive advantage

2. "America First" Reshapes Global Mining Policies

U.S. policy shift

- Ending “friend-shoring”(mineral supply chain alliances) in favor of full domestic reshoring

- Scaling back IRA incentivesfor foreign suppliers, hitting Canada & Australia hardest

- Higher tariffs likely, pushing EU/Japan/Korea to secure independent supply deals(Africa, LATAM)

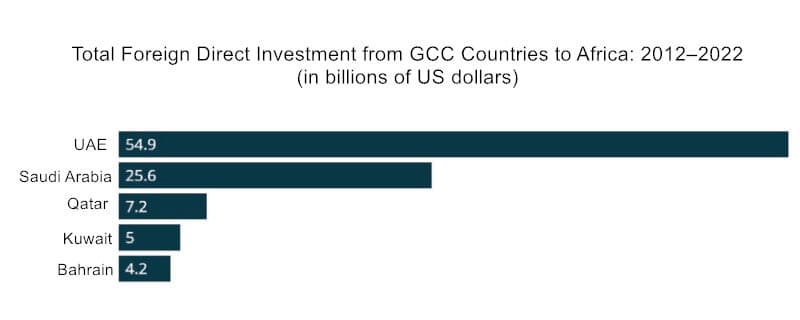

3. Gulf Nations Accelerate Their Mining Expansion

Saudi Arabia, UAE, & Qatar are emerging as major mining players, leveraging:

- Establishing International Platforms: For four consecutive years, Saudi Arabia has hosted the “Future Minerals Forum,” aiming to cultivate it into a premier global hub for mining cooperation and investment.

- Accelerating Cross-Border M&A: Following Saudi Arabia’s acquisition of a 10% stake in the base metals division of Brazil’s Vale in 2024, the three Gulf nations are expected to drive a surge in additional mining investment deals throughout 2025.

- Developing Domestic Resources: In January 2025, Saudi Aramco and the Saudi Arabian Mining Company (Ma’aden) announced the formation of a joint venture. Their objective is to commence domestic lithium production by 2027, thereby securing a pivotal position within the new energy supply chain.

- Acquiring Global Assets: Saudi Arabia is currently planning to acquire an equity stake in Pakistan’s Reko Diq copper-gold mining project. Should the deal be finalized, Saudi Arabia will partner with Canada’s Barrick Gold Corporation and the Government of Pakistan to develop this world-class copper-gold deposit, with initial mining operations projected to commence in 2028.

Key Takeaway: Gulf capital will compete with U.S./EU investors, especially in Africa.

4. Political Instability and Market Volatility

2025 elections & instability in key mining hubs may disrupt supply:

- Europe– Political shifts could delay critical minerals policy coordination

- Africa– Sahel jihadist expansion, coups, and DRC unrest (cobalt/copper)

- Chile, Côte d’Ivoire, Philippines– Election risks for mining policies

5. Surging Resource Nationalism & Legal Risks

Currently, resource nationalism is surging across global frontiers and emerging markets, accompanied by an escalation in policies and tactics—ranging from traditional legislative pressure to more aggressive price controls, and even extreme security threats. Mexico plans to increase mining royalties; Indonesia intends to curb nickel production in an effort to bolster price levels; the DRC is experimenting with export control measures and, as of February, has already suspended cobalt exports; and countries in the Sahel region have witnessed incidents involving the kidnapping of mining executives. Multinational mining corporations face the potential for substantial financial losses stemming from nationalization and tax hikes, while disputes over contract terms and regulatory reforms could trigger a surge in related litigation.

6. Tighter Regulations Reshape M&A Landscape

In 2025, weighed down by persistently high interest rates in Western nations and insufficient government support, the outlook for mergers and acquisitions (M&A) within the mining industry remains subdued. However, the gold sector may prove to be an exception; driven by a dual impetus of sustained high gold prices and dwindling reserves, major gold mining companies could trigger a new wave of M&A activity. Meanwhile, as the energy transition accelerates, copper—a core raw material for the green economy—is expected to become the most active segment within the critical minerals M&A landscape.

Notably, governments worldwide have significantly intensified their scrutiny of mining transactions, particularly those involving critical minerals. This heightened regulatory pressure may compel companies to recalibrate their strategies: on one hand, large-scale cross-jurisdictional M&A deals may face further headwinds; on the other, smaller-scale projects with more manageable risks are likely to gain favor. Joint ventures and strategic partnerships may well emerge as the new industry norm, enabling companies to achieve their commercial objectives while effectively navigating regulatory hurdles and diversifying financial risks.

7. New Trends in ESG Compliance

ESG compliance requirements have consistently remained an unavoidable and critical issue for mining enterprises worldwide. In recent years, the European Union has successively introduced a series of “Green Deal” policy packages, spanning diverse sectors such as climate, energy, transport, and taxation. This increasingly stringent and complex compliance framework has not only significantly raised compliance costs for businesses but has also triggered ripple effects—such as eroding the competitiveness of EU industries and dampening investor confidence. Notably, in February of this year, the European Commission unveiled its first batch of comprehensive simplification measures. These measures address key policies—including the Corporate Sustainability Due Diligence Directive (CSDDD), the Corporate Sustainability Reporting Directive (CSRD), and the Carbon Border Adjustment Mechanism (CBAM)—intending to reduce administrative burdens on businesses and strike a balance between economic growth and the achievement of climate goals. Amendments to the CSRD, in particular, are expected to exempt 80% of businesses from its scope of application.

Furthermore, in October of last year, the Comprehensive Mining Standards Initiative (CMSI)—developed collaboratively by a consortium of global critical minerals associations—launched its first public consultation phase. Its vision is to foster sustainable societal development through the responsible production, sourcing, and recycling of metals and minerals; its objective is to streamline the current landscape of mining standards and drive continuous improvement in ESG practices across the metals and minerals value chain. While there is broad consensus within the industry regarding the necessity of standard simplification, some stakeholders have expressed concerns that the existing framework—such as the Initiative for Responsible Mining Assurance (IRMA)—could potentially be diluted.

Finally, any stagnation—or even regression—on the part of governments and multinational corporations regarding the sustainable development agenda may well prompt civil society groups to exert greater pressure on high-impact industries, including the mining sector.

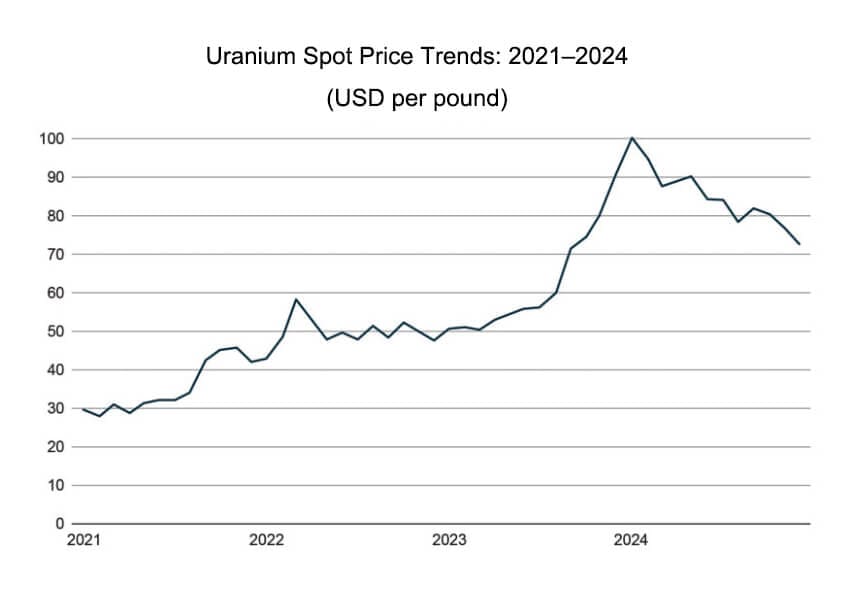

8.Uranium Markets Heat Up With Nuclear Revival

Record-high uranium demand

- 40+ countries expanding nuclear power

- AI data centers driving new energy needs

Supply shifts

- Kazakhstan stays dominant

- Africa rises(Namibia, Niger-Russia deals, Mauritania FID in mid-2025)

9.AI’s Mining Boom (and Risks)

Amidst the wave of digital transformation, Artificial Intelligence (AI) is emerging as a core driving force reshaping the landscape of the mining industry. This disruptive technology is set to deeply permeate the entire mining value chain—from geological exploration and extraction optimization to safety monitoring and environmental assessment—as the application scenarios for AI continue to expand rapidly. The integration of AI with mechanized equipment will help reduce labor-intensive processes and optimize energy efficiency, thereby lowering operational costs. However, the resulting labor displacement effect could exacerbate tensions between mining companies and labor unions. In established mining regions within emerging markets, the mining industry serves as a vital pillar supporting local employment.

The rapid advancement of AI technology also necessitates that companies build internal expertise to mitigate risks such as operational failures and security vulnerabilities. Without professional assessment and effective integration of AI technologies, companies risk adopting AI solutions that are incompatible or harbor inherent security risks. Furthermore, when deploying AI systems, companies must carefully consider compliance issues related to technology trade—particularly in scenarios involving cross-border data transfers and international partnerships. Companies must pay special attention to export controls, sanctions, and other trade restriction policies to avoid penalties or operational constraints resulting from regulatory non-compliance.

10.How the Mining Industry Can Reshape Its Appeal

Finally, the mining industry continues to face formidable existential challenges: how to reshape its public image to maintain its appeal to young talent and investors, while simultaneously winning broad public acceptance. The industry’s image is directly linked to its ability to secure the talent and capital necessary to underpin the energy transition and technological innovation.

In recent years, enrollment rates in mining-related academic programs in Canada and Australia have plummeted. According to a 2024 survey by the World Economic Forum (WEF), 40% of surveyed mining employers believe that a “lack of talent attraction” will hinder their companies’ transformation efforts. This issue is particularly acute in critical areas that will determine the industry’s future—such as AI, robotics, and sustainability.

Concurrently, the reputational risks associated with traditional mining practices continue to deter global investors. In 2025, the “Global Mining Investors Council 2030” alliance is expected to further advance the development of an “environmentally and socially responsible” mining industry; likewise, the Comprehensive Mining Standards Initiative (CMSI)—aimed at promoting responsible production—is anticipated to make substantial progress. While these measures may not yield immediate results, they are expected to gradually bolster confidence in participation within the financial sector.

Conclusion

The mining and metals industry stands at a pivotal crossroads in 2025, facing complex challenges but also unprecedented opportunities. As geopolitical tensions reshape supply chains and ESG requirements become more stringent, industry players must navigate an evolving landscape marked by resource nationalism, technological disruption, and shifting investment patterns. The sector’s ability to balance these competing demands—through strategic partnerships, responsible mining practices, and technological innovation—will determine its success in powering the global energy transition. While risks abound, those who can adapt to the new era of fragmented supply chains, AI integration, and heightened stakeholder expectations will be well-positioned to thrive in this transformed industry landscape. Ultimately, the mining sector must prove it can be both an engine of economic growth and a responsible steward of environmental and social outcomes.